Every American saver planning for retirement faces one critical choice: open a Roth IRA or a Traditional IRA. The two accounts follow opposite tax structures that drastically shift total investment growth over decades of saving.

Most people guess which account wins long-term, relying on generic financial articles without personalized math. Rough estimates fail to account for current tax brackets, future retirement tax rates, annual contributions, investment returns, and age milestones.

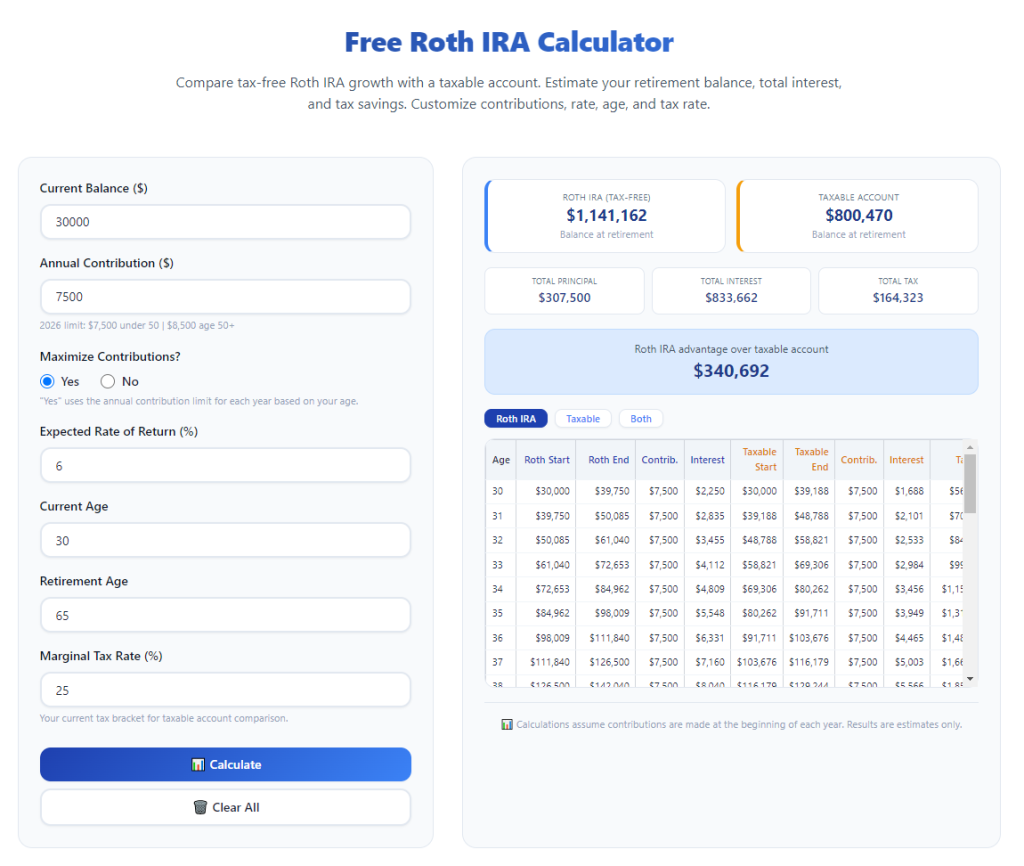

A dedicated Roth IRA calculator compare vs traditional IRA growth eliminates guesswork entirely. This specialized financial tool runs side-by-side growth simulations, factors in all tax rules unique to each IRA type, and outputs clear, personalized balance projections for every savings timeline.

This comprehensive guide breaks down why manual IRA math fails savers, core advantages of using a dedicated comparison calculator, mandatory tool features, real-life use cases, and a complete beginner workflow to run accurate Roth vs Traditional IRA growth comparisons. All content uses plain American financial language, short readable paragraphs, and naturally spaced target keywords for stable Google ranking performance.

Why Manual Roth vs Traditional IRA Growth Math Is Unreliable

Calculating IRA long-term growth by hand or basic spreadsheets creates consistent blind spots that lead to costly retirement planning mistakes. The tax difference between Roth and Traditional IRAs adds multiple layers of complex variables most savers overlook.

Pre-tax vs after-tax contribution math confusion

Traditional IRA contributions reduce your current taxable income, delivering an immediate tax deduction each filing year. Roth IRA deposits come from fully taxed take-home pay with no upfront tax break. Hand calculations rarely balance the upfront tax savings of Traditional IRAs against the lifetime tax-free withdrawals of Roth IRAs.

Ignoring tiered income eligibility rules

Both IRAs impose strict annual income caps on full contribution eligibility. High earners may only partial fund a Roth IRA or lose Traditional IRA deduction eligibility entirely. Basic math cannot auto-adjust contribution limits based on your filing status and adjusted gross income.

Missing mandatory distribution rules

Traditional IRAs force required minimum distributions (RMDs) starting at a fixed retirement age, creating taxable annual withdrawals no matter your cash flow needs. Roth IRAs carry zero RMD rules, letting funds compound tax-free indefinitely if left untouched. Manual growth calculations almost never integrate RMD tax drag into long-term projections.

Failure to model two separate tax brackets

Accurate IRA growth comparison requires entering two tax rates: your current working tax bracket and your predicted retirement tax bracket. Many savers assume identical tax rates during working years and retirement, skewing all final balance totals. A standalone spreadsheet cannot auto-simulate dual tax tier compounding over 30+ years.

Overlooking early withdrawal penalty structures

Each IRA type applies different penalty and tax rules for accessing funds before age 59.5. Traditional IRA early withdrawals trigger full income tax plus a 10% penalty. Roth IRA principal withdrawals stay penalty-free, while earnings early withdrawals incur standard penalties. Manual growth estimates ignore liquidity cost differences that alter net growth if you tap funds mid-career.

Core Benefits of a Roth IRA Calculator Compare vs Traditional IRA Growth

Integrating a purpose-built Roth IRA calculator compare vs traditional IRA growth into your retirement planning workflow delivers precise, actionable financial insights generic savings tools cannot match. Every advantage directly addresses the flaws of manual comparison methods.

Side-by-side tax-adjusted growth projections in real time

The core function of this specialized calculator is parallel growth modeling. It runs identical annual contribution, return, and timeline inputs through both Roth and Traditional IRA tax frameworks simultaneously. You view net after-retirement withdrawal balances for each account on one unified report, removing all manual cross-comparison work.

Automatically accounts for all official IRS IRA rules

Top-tier comparison calculators embed up-to-date IRS contribution limits, income phase-out ranges, RMD schedules, early withdrawal penalties, and tax classification logic. You avoid researching annual regulatory updates or manually adjusting formulas when contribution caps or tax brackets shift.

Personalizes results to your unique financial profile

Generic retirement calculators use one-size-fits-all tax assumptions. This dedicated IRA comparison tool customizes every projection around your filing status, current salary, annual IRA deposit amount, target retirement age, average portfolio return rate, and predicted post-retirement tax bracket.

Quantifies total lifetime tax difference between the two IRAs

A key output exclusive to a Roth IRA calculator compare vs traditional IRA growth is a clear lifetime tax tally. It sums upfront Traditional IRA tax deductions against decades of Roth tax-free growth, showing exactly how much total tax you pay under each savings route over your full retirement timeline.

Supports flexible "what-if" scenario testing

You can instantly tweak single variables to test alternate financial plans: raise annual contributions, adjust expected market returns, push back retirement age, or switch predicted retirement tax brackets. Each edit refreshes both Roth and Traditional growth curves in seconds for instant scenario comparison.

Simplifies long-term compound growth visualization

Most comparison calculators generate year-by-year breakdown tables or simple growth charts. You track annual account balances for both IRA types from your first deposit through full retirement, making compound tax advantages easy to visualize instead of abstract math.

Must-Have Features in a Quality Roth IRA Calculator Compare vs Traditional IRA Growth

Not all dual IRA growth calculators deliver accurate, usable results. When selecting a tool to run your retirement projections, confirm it includes these IRA-specific built-in functions critical for trustworthy comparisons.

Dual input fields for current and retirement marginal tax brackets

Without two separate tax rate entry boxes, the calculator cannot replicate the core tradeoff between Traditional IRA immediate tax relief and Roth IRA permanent tax exemption. This feature is non-negotiable for valid growth comparison.

Built-in IRS contribution limit auto-capping

The tool must automatically restrict annual Roth and Traditional IRA contributions to official annual maximums, including catch-up contribution thresholds for savers age 50 and older. Manual entry calculators let users input unrealistic deposit amounts that skew all growth data.

Filing status and AGI income phase-out logic

Quality calculators include dropdowns for single, married filing jointly, head of household, and separate filer statuses. They apply income-based contribution phase-outs automatically so projections reflect how much you can legally fund each IRA annually.

Adjustable investment annual return slider

Look for a customizable average annual return input, ranging from conservative low-risk portfolios to higher-growth stock-heavy allocations. Compound growth gaps between Roth and Traditional IRAs widen significantly with higher long-term market returns.

Full RMD tax simulation for Traditional IRA balances

The calculator must calculate annual required minimum distributions starting at the mandatory age, add those taxable withdrawals to your retirement tax burden, and subtract tax costs from final net Traditional IRA value. Roth IRA projections exclude all RMD deductions by design.

Early withdrawal penalty modeling toggle

A flexible penalty simulation feature lets you test scenarios where you access savings before full retirement age. It separates Roth principal penalty-free withdrawals from taxable earnings withdrawals to show true net growth impact for both accounts.

Year-by-year breakdown export capability

Top comparison calculators generate downloadable year-by-year balance tables for both IRAs. This detailed output lets you audit compound growth, tax charges, and contribution totals for every year of your savings journey.

Scenario save and duplicate function

For multi-test financial planning, the tool should let you save baseline calculations and duplicate scenarios to tweak individual variables without retyping your entire financial profile from scratch.

Common Real-World Use Cases for a Roth IRA Calculator Compare vs Traditional IRA Growth

This specialized comparison tool serves every type of saver, from young entry-level workers to mid-career professionals and near-retirement planners adjusting long-term savings strategies.

Young early-career savers with low current tax brackets

Workers in their 20s and early 30s often sit in low marginal tax brackets today, expecting higher taxable income once they retire. Running projections via a Roth IRA calculator compare vs traditional IRA growth clearly demonstrates Roth’s tax-free compounding advantage for this demographic.

Mid-career high-income professionals

High earners face Roth IRA income phase-out limits and lose full Traditional IRA deduction eligibility. The calculator auto-limits contribution amounts for each account and compares partial Roth funding versus non-deductible Traditional IRA growth to pick the higher-net-value option.

Savers planning early semi-retirement before full RMD age

Anyone targeting partial retirement in their 50s needs to model early fund access rules. The calculator contrasts penalty-free Roth principal withdrawals against fully taxed Traditional IRA early distributions to measure long-term growth erosion from mid-career withdrawals.

Near-retirement planners rebalancing existing IRA assets

Saver approaching their late 50s can input their current existing Roth and Traditional IRA balances into the calculator. The tool projects remaining compound growth, RMD tax costs, and net spendable retirement funds to guide asset reallocation decisions.

Married couples filing joint tax returns

Joint filers benefit heavily from the calculator’s filing status module. It applies joint income phase-out rules, combined contribution limits, and dual household tax bracket projections to compare household-level Roth versus Traditional IRA combined growth totals.

Investors testing aggressive vs conservative portfolio allocations

By adjusting the annual return slider, users model how higher market growth amplifies the tax-free compounding gap of Roth IRAs relative to taxable Traditional IRA withdrawals in later life. Conservative low-return portfolios narrow this growth difference dramatically.

Financial advisors building client retirement illustrations

Professional planners rely on the calculator’s side-by-side growth reports to show clients tangible numerical differences between the two IRA structures, removing subjective financial advice in favor of personalized tax-adjusted math.

Step-by-Step Complete Workflow: Use a Roth IRA Calculator Compare vs Traditional IRA Growth

Follow this structured, beginner-friendly process to input your financial data, generate accurate dual IRA growth projections, and interpret the comparison results to pick your optimal retirement savings account.

Step 1: Gather all required personal financial data first

Before opening the comparison calculator, compile every data point the tool requires to avoid incomplete, skewed projections:

- Current annual gross household income and tax filing status

- Your current marginal federal income tax bracket

- Predicted federal tax bracket you expect during full retirement

- Planned annual dollar amount you can contribute to an IRA each year

- Your current age and target full retirement age

- Average annual investment return you expect from your IRA portfolio

- Existing balances in any current Roth or Traditional IRA accounts (if applicable)

- Whether you will need to withdraw partial funds before age 59.5

Step 2: Launch the dedicated Roth vs Traditional IRA growth comparison calculator

Open the specialized tool built for Roth IRA calculator compare vs traditional IRA growth functionality. Skip generic all-purpose retirement calculators that lack built-in IRA tax and rule logic. Navigate directly to the dual-side comparison input dashboard.

Step 3: Enter core personal and tax profile inputs

Fill out the foundational profile section in order:

- Select your tax filing status from the dropdown menu

- Input your current annual adjusted gross income

- Type your current working marginal tax rate percentage

- Enter your estimated retirement marginal tax rate percentage

- Input your current age and target retirement age numbers

The calculator will instantly apply IRS income phase-out rules and contribution cap limits behind the scenes based on your entries.

Step 4: Input annual IRA contribution and catch-up details

Navigate to the contribution input panel:

- Enter the maximum yearly dollar amount you plan to deposit into an IRA

- Toggle the age 50+ catch-up contribution switch if you qualify for extra annual deposits

- Add any existing pre-existing Roth IRA and Traditional IRA current balances into their separate dedicated fields

The tool automatically caps your entered contributions to match legal annual IRS limits, eliminating unrealistic deposit inputs that distort growth math.

Step 5: Set portfolio growth and early withdrawal parameters

Adjust the investment and liquidity rule sliders to match your personal plan:

- Move the average annual portfolio return slider to match your expected long-term market gains

- Toggle the early withdrawal scenario switch if you plan to access funds before age 59.5

- If enabling early withdrawals, input the age and annual dollar amount of any planned pre-retirement fund access

Step 6: Run the side-by-side Roth vs Traditional IRA growth comparison calculation

Double-check all entered numbers for typos or missing values, then select the “Generate Growth Comparison” main action button. The tool will process both IRA growth models simultaneously in under ten seconds.

Step 7: Review the core dual growth summary dashboard

Start analysis with the high-level comparison overview panel, which displays three critical paired metrics:

- Total projected account balance (before retirement tax withdrawals) for Roth IRA vs Traditional IRA

- Total lifetime federal tax paid across the full savings timeline for each account type

- Net after-tax spendable retirement funds remaining after all required withdrawals and tax charges

Note the raw growth gap between the two IRA totals and the total lifetime tax difference highlighted on the summary page.

Step 8: Dive into year-by-year detailed breakdown tables

Scroll down to access the separate annual breakdown tables for Roth IRA and Traditional IRA growth. Review each table to identify:

- Annual deposit amounts applied each year

- Yearly investment compound growth gains

- Tax deductions applied to Traditional IRA contributions during working years

- RMD taxable withdrawal charges subtracted from Traditional IRA balances post-retirement

- Cumulative net tax-free value retained in the Roth IRA through all retirement years

Cross-reference matching years on both tables to see annual growth differences compound over decades.

Step 9: Run alternate “what-if” scenario tests

Duplicate your baseline calculation to test adjusted financial plans without erasing your original data:

- Raise or lower your annual IRA contribution amount

- Shift your predicted retirement tax bracket higher or lower

- Adjust the portfolio average annual return rate up or down

- Toggle early withdrawal rules on or off to measure liquidity growth impact

Each duplicated scenario refreshes both Roth and Traditional growth curves instantly for direct side-by-side scenario comparison.

Step 10: Export and save your finalized comparison report

Once you finish testing all relevant financial scenarios, locate the export function to download the complete comparison report. The saved document contains the summary growth totals, full year-by-year breakdown tables, and all input assumptions you entered for future reference during tax and retirement planning reviews.

Step 11: Finalize your IRA savings decision based on net after-tax totals

Base your account choice on the net spendable after-retirement funds metric, not raw pre-tax account balances. A higher raw Traditional IRA balance often disappears once mandatory taxable RMD withdrawals are subtracted, while Roth IRA totals remain fully tax-free for all lifetime withdrawals.

Common Costly Mistakes When Using a Roth IRA Calculator Compare vs Traditional IRA Growth

Even with a fully featured comparison tool, these frequent user errors produce unreliable growth projections and lead to poor IRA selection decisions. Avoid each pitfall to keep your retirement math accurate.

Entering identical current and retirement tax brackets

Most savers incorrectly input the same tax rate for working years and retirement. This erases the core tax tradeoff the calculator is designed to measure. Always use a realistic lower or higher predicted post-retirement tax bracket based on your expected retirement income streams.

Ignoring income phase-out contribution caps

Users often input maximum IRA annual deposits without checking if their AGI triggers Roth IRA phase-outs or Traditional IRA deduction limits. The calculator auto-limits contributions, but failing to review the phase-out warning leads to misinterpreting final growth totals.

Disregarding RMD tax simulation for Traditional IRA balances

Many planners only focus on pre-retirement raw growth numbers and overlook the mandatory taxable RMD withdrawals that drain Traditional IRA value after retirement age. Always evaluate net after-RMD spendable funds as your primary comparison metric.

Using overly optimistic long-term portfolio return rates

Overinflating average annual investment returns widens the Roth IRA growth advantage artificially, creating unrealistic projections. Stick to historical market baseline return ranges matching your actual portfolio risk level.

Skipping duplicate what-if scenario testing

Relying on only one baseline calculation hides how shifting income, tax, or contribution variables flip which IRA delivers superior long-term growth. Always test multiple alternate financial plans before finalizing your savings strategy.

Forgetting to input existing IRA account balances

Users starting with pre-funded Roth or Traditional IRA assets who skip entering current balances produce incomplete growth curves. The calculator cannot model combined legacy and new contribution compound growth without opening balance data.

Misinterpreting raw account balance over net after-tax value

Raw total account size numbers do not reflect real spendable cash in retirement. Traditional IRA balances carry future tax liabilities on every dollar withdrawn, while all Roth IRA funds remain tax-free. Prioritize net after-tax totals for all comparisons.

Pro Expert Tips to Maximize Accuracy From Your Roth IRA Calculator Compare vs Traditional IRA Growth

Use these financial planning best practices to refine your calculator inputs and generate the most trustworthy, personalized IRA growth comparisons for your retirement roadmap.

- Refresh your AGI and tax bracket data each tax filing year to update calculator baseline inputs, as income shifts directly alter IRA contribution eligibility and tax savings math.

- Run new growth projections every 3–5 years as you advance through career stages, adjust retirement timelines, or shift investment portfolio risk levels.

- Split your scenario testing into low, moderate, and high retirement tax bracket cases to build a range of possible IRA growth outcomes instead of relying on one single prediction.

- Factor other retirement income sources (pensions, taxable brokerage accounts, rental income) into your predicted retirement tax bracket to avoid underestimating post-career tax rates.

- Separate short-term emergency savings goals from long-term IRA growth projections; the calculator’s early withdrawal toggle quantifies how tapping IRA funds mid-career erodes decades of compound tax-free growth.

- Save all exported comparison reports in a dedicated retirement planning folder to track shifting IRA growth projections over multiple years of income and market changes.

- Cross-reference calculator contribution limit outputs against official annual IRS IRA publications to confirm the tool’s embedded regulatory data stays current with new tax rules and caps.

- For joint household planning, run dual individual calculator sessions for each spouse, then combine the two sets of Roth and Traditional growth totals to measure full household retirement savings performance.

Final Thoughts

Choosing between a Roth IRA and Traditional IRA ranks among the most impactful financial decisions for long-term retirement wealth building. The opposing pre-tax and after-tax tax structures create massive gaps in total compound growth over 20, 30, or 40 years of consistent saving.

Manual spreadsheets and generic retirement calculators lack the layered IRS rule logic and dual tax simulation needed to produce trustworthy side-by-side growth comparisons. A dedicated Roth IRA calculator compare vs traditional IRA growth removes all guesswork by embedding official IRA regulations, personalized tax modeling, and parallel compound growth projections for both account types in one unified tool.

By following the complete step-by-step input and analysis workflow outlined above, avoiding common user calculation mistakes, and running multiple what-if financial scenarios, you generate fully personalized net after-tax retirement growth totals. These clear, data-backed results eliminate subjective financial guesswork and let you select the IRA structure that delivers the maximum spendable wealth for your unique income, tax, savings, and retirement timeline profile.

Whether you are a young first-time saver, mid-career professional rebalancing assets, or near-retirement planner refining your withdrawal strategy, this specialized comparison calculator turns complex IRA tax and compound growth math into simple, actionable retirement planning insights that align with your long-term financial goals.

After learning the operation method, click the link below to enter the tool page for immediate use.