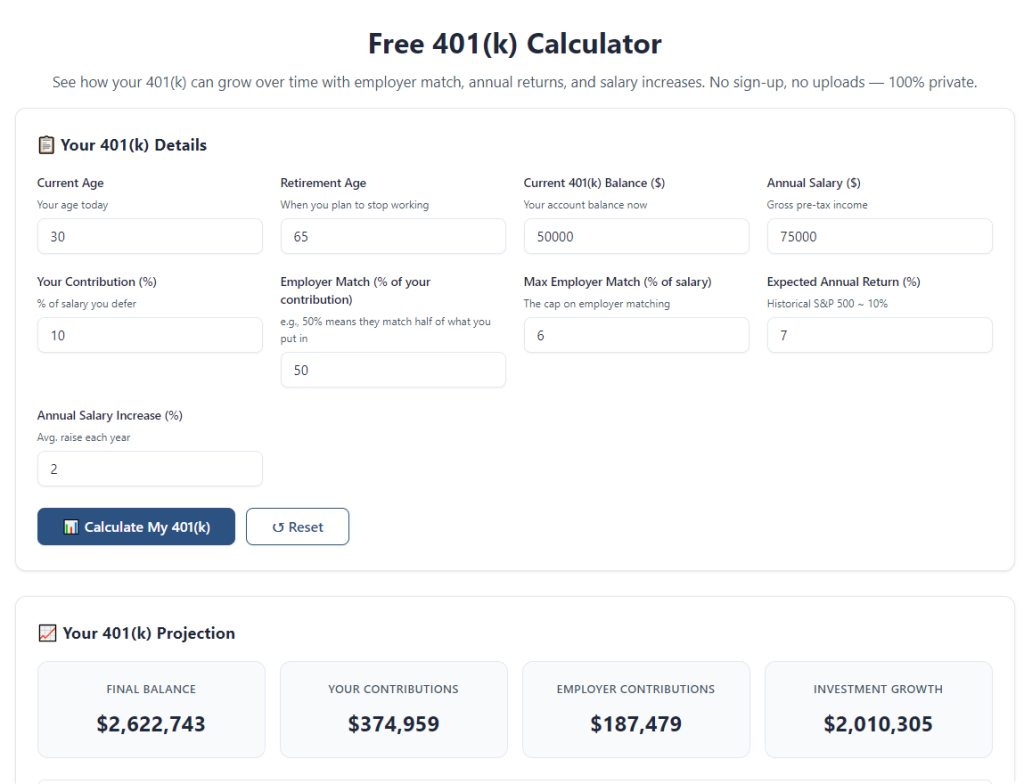

If you’ve hit age 50 or will cross that milestone soon, your 401(k) plan unlocks special catch-up contribution rules designed to speed up retirement savings growth. Most regular retirement calculators ignore these extra allowed deposits, leaving you with wildly inaccurate projections for your post-work nest egg.

Many mid-career and late-career savers make costly planning mistakes because they can’t separate standard annual contribution caps from the extra catch-up amounts reserved for anyone 50 or older. Guessing how much extra you can set aside, and how compound interest amplifies those extra dollars, leads to underfunded retirement plans and last-minute financial stress.

Manual spreadsheet math to model catch-up contributions is error-prone and time-consuming. You have to track yearly IRS limits, adjust for your current age, input employer matching rules, and factor in market growth rates all at once. A dedicated 401 (k) calculator with catch-up contributions over 50 eliminates all guesswork by building age-based catch-up rules directly into its core formulas.

This complete, beginner-friendly tutorial breaks down everything you need to know. We cover the flaws of generic retirement calculators, unique benefits of catch-up enabled 401(k) tools, mandatory core features, real-world planning use cases, and a detailed step-by-step workflow to run accurate savings forecasts tailored to savers aged 50 and above.

H2: Why Generic 401(k) Calculators Fail Savers Over Age 50

Standard free retirement calculators built for all age groups lack specialized logic for catch-up contributions, creating major gaps in your long-term financial planning. These limitations leave people 50+ with unreliable, lowball retirement balance estimates.

Generic Tools Omit Official Catch-Up Contribution Rules

The IRS sets separate annual maximums for regular employee 401(k) deposits and additional catch-up funds available only once you turn 50. Basic calculators only pull the baseline yearly limit and have no field to input extra catch-up savings. If you plug in your actual total yearly contributions (regular + catch-up), generic tools flag your input as over the legal cap and skew all growth numbers.

No Age-Based Automatic Catch-Up Eligibility Triggers

Many savers start partial catch-up deposits the year they turn 50 and ramp up full catch-up amounts in subsequent years. Regular calculators cannot auto-adjust contribution limits based on your current age, planned retirement age, or the exact year you hit fifty. You must manually recalculate every single year’s allowed maximums on your own, which opens the door to arithmetic mistakes.

Separate Modeling for Employer Matching Is Missing

Employer match formulas rarely account for catch-up deposits. Most companies only offer matching funds against your standard pre-401(k) contributions, not the extra catch-up portion for savers over 50. Generic calculators apply matching percentages to all your deposits equally, overestimating your total employer funds and creating unrealistic growth projections.

No Side-by-Side Catch-Up vs. No Catch-Up Comparison

To build an effective savings strategy, you need to see two clear forecasts: one where you take full advantage of annual catch-up limits after 50, and one where you skip extra deposits entirely. Standard calculators only generate a single projection, forcing you to run separate manual calculations and compare results on your own.

Complex Compound Interest Math Takes Hours to Recalculate Manually

Catch-up contributions add thousands in extra principal each year, and compound market returns multiply that gap over 10, 15, or 20 years until retirement. Recreating this multi-year compound growth by hand or basic spreadsheets requires dozens of formula updates every time you adjust your contribution percentage, income, or expected investment return rate.

H2: Core Advantages of Using a 401 (k) Calculator With Catch-Up Contributions Over 50

Switching to a specialized 401 (k) calculator with catch-up contributions over 50 streamlines your entire retirement planning process while delivering hyper-accurate projections built around IRS age-based savings rules. Every feature is engineered specifically for savers entering their final decades of work.

Built-In IRS Catch-Up Limit Compliance Logic

These niche calculators preload current official annual contribution caps, split between baseline employee deposits and age 50+ catch-up allotments. The tool automatically validates your input amounts to ensure you never model illegal over-contributions and clearly labels how much of your yearly savings counts as standard versus catch-up funding.

Age-Tiered Contribution Auto Adjustment

Input your current age and target retirement age once, and the calculator instantly switches its limit framework the calendar year you turn fifty. It will model lower pre-50 savings caps for your early career years, then raise the allowed total contribution ceiling for every year you remain employed after hitting the age milestone.

Separate Employer Match Calculation for Standard vs. Catch-Up Funds

The tool includes dedicated fields to input your employer’s matching policy, plus a toggle to define whether matches apply only to baseline contributions or extend to catch-up deposits. It splits your annual deposits into two buckets and calculates matching dollars correctly, eliminating inflated balance estimates common with generic planners.

Dual Scenario Side-by-Side Forecasting

The biggest value add for late-career savers is the dual projection view. You can generate two parallel reports: one with maximum catch-up contributions each year after age 50, and one without any extra catch-up savings. The calculator highlights the total dollar difference in your final retirement nest egg to show the tangible long-term impact of catch-up deposits.

Full Customization for All Late-Career Financial Variables

You can adjust every critical planning input without breaking the catch-up calculation logic: annual salary raise percentages, expected average market rate of return, existing 401(k) account balance, planned yearly contribution percentage, and partial catch-up deposits if you cannot afford the full allowed extra amount each year.

Saves Hours of Manual Spreadsheet Maintenance

Instead of building multi-year compound interest tables and updating contribution limits annually, you input your data once and refresh projections in one click. This frees up time to focus on other parts of your financial plan, like Roth conversions, healthcare savings, and post-retirement expense budgeting.

Clear, Actionable Output for Adjusting Your Payroll Deductions

After running your calculation, the tool generates simple breakdowns showing exactly how much extra to deduct from each paycheck to hit full annual catch-up limits. You can take these figures directly to your HR department to adjust your 401(k) withholding percentages mid-year or during open enrollment windows.

H2: Must-Have Features in a Quality 401 (k) Calculator With Catch-Up Contributions Over 50

Not every retirement calculator that mentions catch-up rules delivers accurate, usable results for savers aged 50 and older. The most reliable 401 (k) calculator with catch-up contributions over 50 includes these non-negotiable, late-career focused features.

Split Contribution Input Fields (Standard vs. Catch-Up)

Look for a tool that separates your yearly baseline employee contribution and your age-eligible catch-up contribution into distinct input boxes. Avoid calculators that force all savings into a single field, as these cannot properly isolate catch-up funds for matching and limit validation calculations.

Age Eligibility Slider or Numeric Input

A dedicated age entry box triggers the catch-up formula automatically once your age hits fifty. Premium tools even let you test hypothetical scenarios, such as “what would my balance look like if I start catch-up deposits two years after turning 50” or “what if I retire the same year I turn fifty.”

Employer Match Customization Toggle

The calculator must include a setting to disable matching on catch-up contributions, which aligns with the rules of most corporate 401(k) plans. It should display a clear line item showing total employer matching funds per year, separated from your personal standard and catch-up deposits.

Adjustable Investment Return and Volatility Ranges

Late-career savers often shift to more conservative asset mixes as retirement draws near. Top-tier calculators let you input low, moderate, and high average annual return rates and recalculate catch-up growth projections for each risk profile.

Multi-Year Year-by-Year Breakdown Table

A detailed yearly breakdown table is essential. It should display each calendar year’s standard contribution, catch-up contribution, employer match, interest growth, and running total account balance. This table makes it easy to spot exactly which years catch-up deposits add the most compound value.

Dual Comparison Reporting (Catch-Up Enabled vs. Disabled)

Without a direct side-by-side comparison, you cannot quantify the financial benefit of prioritizing extra savings after age fifty. The calculator should generate a one-page summary showing total account value difference at retirement between the two scenarios.

No Hidden Paywalls for Core Catch-Up Calculations

Avoid tools that lock age 50+ catch-up modeling behind premium subscriptions. The core functionality—limit validation, dual projections, yearly breakdown tables—should be accessible to all users without mandatory sign-ups or paid upgrades.

H2: Real-World Use Cases for a 401 (k) Calculator With Catch-Up Contributions Over 50

This specialized retirement planning tool fits every common financial scenario for anyone approaching or past their 50th birthday, whether you work full-time, part-time, or plan phased retirement.

Mid-Career Savers Catching Up After Late 401(k) Enrollment

Many Americans delay consistent 401(k) contributions until their 40s, leaving a smaller starting nest egg by age fifty. The calculator models how full annual catch-up deposits can close that savings gap over your final working decade and hit your target retirement balance.

Employees Planning Open Enrollment Payroll Adjustments

During yearly benefits open enrollment, savers over 50 use the calculator to test different withholding percentages. You can input your target standard contribution plus full catch-up amounts and see exactly how much each paycheck will decrease, to avoid unmanageable monthly cash flow strain.

Phased or Partial Retirement Planning

If you plan to reduce hours or switch to part-time work after age 50, your annual income and ability to fund catch-up deposits will drop. The calculator lets you lower contribution amounts in specific future years and recalculate long-term growth without invalidating age-based catch-up logic.

Comparing Catch-Up 401(k) vs. IRA Extra Contributions

Many savers over fifty have catch-up options for both workplace 401(k) accounts and personal IRAs. You can run separate calculator projections for each vehicle to decide whether prioritizing extra 401(k) deposits delivers stronger tax-deferred compound growth for your timeline.

Pre-Retirement Financial Advisor Meeting Prep

Before consulting a financial planner, generate a full dual-scenario report from the calculator to bring to your appointment. The year-by-year breakdowns give your advisor concrete data to refine your asset allocation and savings targets for your remaining working years.

Testing Partial Catch-Up Contribution Budgets

Not every saver can afford the full annual catch-up limit immediately after turning fifty. The calculator supports partial catch-up inputs, so you can model gradual increases in extra deposits year over year as your disposable income rises.

Updating Old Retirement Projections After Turning 50

If you ran generic retirement calculators in your 40s, those projections ignored catch-up eligibility. Re-running your numbers on a catch-up specialized tool updates your forecast to reflect the higher yearly contribution maximums available to you now that you qualify.

H2: Step-by-Step Guide to Using a 401 (k) Calculator With Catch-Up Contributions Over 50

Follow this structured workflow to input your financial data correctly, validate catch-up contribution limits, generate accurate growth projections, and turn calculator results into actionable retirement savings adjustments.

Step 1: Gather All Required Financial Input Data First

Before opening the calculator, compile every number the tool will request to avoid incomplete or inaccurate projections. Collect:

- Your current age and exact year you will turn fifty (if not already 50+)

- Your planned full retirement age and total remaining working years

- Current total balance held in your active 401(k) account

- Current annual gross salary and expected average yearly pay raises

- Standard percentage of income you currently contribute to your 401(k)

- Full details of your employer’s matching program (percentage match, contribution cap, match eligibility rules for catch-up funds)

- Expected average annual investment return based on your asset mix (conservative, moderate, aggressive)

- How much extra catch-up funding you can afford each year (full IRS limit or partial deposits)

Step 2: Launch the Specialized Catch-Up 401(k) Calculator

Open the tool in your browser and navigate directly to the main input dashboard. Skip generic retirement planning pages that do not feature dedicated catch-up contribution fields for savers over age fifty. Locate the clearly labeled sections for current age, retirement timeline, standard contributions, and catch-up deposits reserved for users 50+.

Step 3: Input Core Personal Timeline Details

Fill in your current age first—this triggers the tool’s built-in IRS contribution limit logic to activate catch-up fields automatically once your age threshold hits fifty. Next, enter your target retirement age to define the total number of years the calculator will model compound growth for both standard and catch-up savings.

Step 4: Enter Existing 401(k) Balance and Income Metrics

Add your most recent total account balance as the starting principal for all growth calculations. Input your current yearly gross salary and average projected annual raises; the tool will scale your standard contribution amounts upward alongside your income over time.

Step 5: Configure Standard Baseline 401(k) Contribution Settings

Enter the percentage of your salary you allocate to regular yearly 401(k) deposits. The calculator will cross-reference this input against the current IRS baseline maximum and flag any overages before you move to the catch-up section.

Step 6: Input Catch-Up Contribution Amounts for Ages 50 and Older

Navigate to the dedicated catch-up contribution input block. Choose between two modes: full automatic yearly catch-up limit based on IRS rules, or custom partial catch-up dollar amounts if you cannot afford the maximum allowed extra deposit each year. The tool will separate these funds entirely from your baseline contributions for matching and growth calculations.

Step 7: Adjust Employer Matching Rules for Catch-Up Eligibility

Locate the employer match configuration panel. Input your company’s matching percentage and maximum match cap. Toggle the key setting that defines whether matching funds apply only to standard contributions or extend to your catch-up deposits over age fifty. This step eliminates overinflated total balance projections common on generic calculators.

Step 8: Set Expected Investment Return Rate Ranges

Input your anticipated average annual market return based on your portfolio’s risk level. For late-career savers shifting to conservative bonds and index funds, select lower return assumptions to generate realistic, non-overoptimistic retirement balance forecasts.

Step 9: Generate Dual Scenario Projections (Catch-Up On vs. Catch-Up Off)

Select the side-by-side comparison report function and click the calculate button. The tool will run two complete multi-year growth models simultaneously: one that includes all your input catch-up contributions every year after age fifty, and one that excludes any extra catch-up deposits entirely. Wait a few seconds for the full yearly breakdown tables and summary totals to load.

Step 10: Review Year-by-Year Breakdown and Final Nest Egg Difference

Start with the high-level summary that displays the total dollar gap between your two retirement balance outcomes. Then scroll through the annual breakdown table to examine how each year’s standard deposit, catch-up deposit, employer match, and investment returns add to your running account balance. Note the calendar years where catch-up contributions create the largest compound value gains.

Step 11: Adjust Inputs to Test Alternative Savings Strategies

Tweak one variable at a time to run what-if planning scenarios:

- Raise or lower your partial catch-up contribution amounts to match monthly cash flow limits

- Shift your retirement age forward or backward to see how extra working years amplify catch-up growth

- Modify your standard payroll contribution percentage alongside catch-up deposits

- Adjust your expected investment return rate to model conservative or bullish market performance

After each change, re-run the dual comparison report to track how your final projected retirement balance shifts up or down.

Step 12: Export or Record Key Figures for Actionable Planning

Save the full calculator report details to a document or notebook for reference during benefits open enrollment or financial planning sessions. Note the exact biweekly or monthly payroll deduction needed to hit your combined standard plus catch-up contribution targets. Use these figures to submit updated withholding forms to your HR team to activate full catch-up savings for the upcoming plan year.

H2: Common Mistakes to Avoid When Using a 401 (k) Calculator With Catch-Up Contributions Over 50

Even with a specialized catch-up enabled 401(k) calculator, these frequent planning errors can skew your projections and lead to flawed retirement savings decisions for savers age 50 and older.

Combining Standard and Catch-Up Deposits Into One Single Input Field

Never merge your baseline yearly contributions and age 50+ catch-up funds into a generic total contribution box. This disables the tool’s matching separation logic and IRS limit validation, resulting in inaccurate employer match calculations and unregulated over-contribution modeling. Always use the split dedicated input sections for each deposit type.

Ignoring Employer Match Rules for Catch-Up Funds

Many users assume their company’s matching program applies equally to standard and catch-up deposits. Most corporate plans exclude catch-up contributions from matching eligibility. Failing to toggle the match restriction setting will overestimate your total employer funding and inflate your projected retirement balance significantly.

Using Overly Optimistic Long-Term Investment Return Rates

Late-career portfolios typically reduce exposure to high-growth volatile stocks as retirement approaches. Inputting aggressive 8% to 10% average annual returns for a conservative post-50 asset mix creates unrealistic growth projections that set unachievable savings expectations. Stick to moderate or conservative return assumptions for ages 50+.

Forgetting to Recalculate After Salary Increases or Hours Reductions

A single calculator run only reflects your current income level. If you receive a substantial raise or shift to part-time work after age fifty, your ability to fund full catch-up deposits changes drastically. Failing to re-run projections with updated salary data leaves your long-term forecast outdated.

Skipping the Dual Comparison Scenario View

Many savers only generate a single projection with catch-up contributions enabled, with no baseline comparison to see the tangible financial cost of skipping extra savings. Without the side-by-side report, you cannot quantify the massive compound value lost by ignoring age 50+ catch-up eligibility.

Modeling Catch-Up Contributions Starting Before Your 50th Birthday

The IRS strictly restricts catch-up deposits to the calendar year you turn fifty and all subsequent years. Inputting catch-up amounts for years prior to your 50th birthday violates official contribution limits and generates invalid, non-compliant savings projections the calculator cannot validate correctly.

H2: Pro Tips to Maximize Accurate Planning With a 401 (k) Calculator With Catch-Up Contributions Over 50

Use these expert financial planning tactics to extract the most valuable, actionable insights from your catch-up enabled 401(k) calculator and build a stronger late-career retirement savings strategy.

- Run calculator projections every six months, especially before annual benefits open enrollment, to adjust catch-up withholding percentages to match changes in your household disposable income.

- Test three distinct return rate tiers (conservative, moderate, aggressive) for your asset mix to build a range of possible retirement balance outcomes instead of relying on a single number.

- Separate your catch-up contribution testing into short-term (5 years until retirement) and long-term (15+ years until retirement) timelines to see how compound interest magnifies extra savings over longer working windows.

- Cross-reference calculator yearly contribution totals against official IRS annual limits to confirm your standard plus catch-up combined deposits stay fully compliant with federal retirement plan rules.

- Pair your 401(k) catch-up calculator projections with IRA catch-up modeling to compare the tax-deferred growth benefits of allocating extra savings to each retirement vehicle.

- Save every dual-scenario comparison report in a dedicated planning folder to track how your projected retirement nest egg grows as you increase catch-up deposits year over year.

- Share your finalized calculator breakdown tables with a licensed financial planner to align your catch-up savings strategy with other retirement vehicles, healthcare savings accounts, and tax planning goals.

H2: Final Thoughts

Catch-up contribution rules for savers age fifty and older represent one of the most powerful tools available to close retirement savings gaps before leaving the workforce. Generic retirement calculators lack the specialized logic needed to model these extra deposits accurately, leaving millions of late-career Americans with flawed, underinformed financial projections.

A trusted 401 (k) calculator with catch-up contributions over 50 eliminates all manual guesswork, IRS limit math errors, and employer matching miscalculations that derail standard retirement planning tools. Its split contribution fields, age-triggered catch-up eligibility logic, and dual side-by-side growth comparisons deliver transparent, realistic forecasts tailored exclusively to anyone past their 50th birthday.

When used following the step-by-step workflow outlined above, this calculator turns abstract retirement math into concrete payroll adjustment actions you can implement immediately through your workplace benefits program. By consistently modeling full or partial catch-up contributions and reviewing the long-term compound value difference year after year, you can build a far larger, more secure nest egg to support your post-work lifestyle without unnecessary financial stress.

Whether you are just approaching fifty, already well into your sixth decade of work, or planning phased partial retirement, integrating this catch-up specialized calculator into your regular financial review routine ensures you never overlook the critical tax-advantaged savings opportunity built into federal 401(k) rules for older employees.

After learning the operation method, click the link below to enter the tool page for immediate use.